Is DeFi real? Yes. Does it work globally? Absolutely, by definition. How about financial inclusion? Hmmm, wait.

All of us are curious learners in our own ways. Not bad for an opening sentence? Now that I have you, I wanted to promote my podcast (a.k.a. The Curious Learners) before I lose anyone further below.

William Arthur Ward says “Curiosity is the wick in the candle of learning.”

Some of us take it far. I generally try. Last year, I decided to do a PhD and study decentralized finance. Having been in financial services in the last decade with experience in operating, investment banking and finally investing in fintech and crypto in the last four years, I wanted to go deeper.

My PhD research proposal was about connecting traditional finance with decentralized finance and how to address financial inclusion. I got admitted to one of the leading research programs in Europe, however I ended up not taking the offer as the school policy didn’t allow me to do it remotely from London (unfortunately the decentralized spirit isn’t widespread enough yet)

In my view, decentralized finance is an extension of the transformation of financial services that have been taking place for the last couple of decades. It started with digitalisation of course and impacted mostly the way products and services are distributed to end-users (either individuals or corporates). Since a few years, we started to see a new chapter in the form of decentralization.

What is DeFi?

DeFi could be summarized as the underlying framework in which financial services and products are made accessible to everyone with none or minimal intermediary services. This in turn ideally leads to increased efficiency, reduced friction and cost and a much larger outreach. This is unfortunately not happening yet at scale as we are in the early innings of this significant transformation. It is the subject of another article.

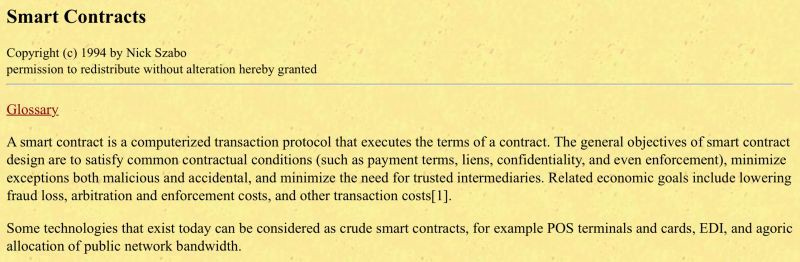

Such abstraction of intermediary is achieved by smart contracts. Ok, but what is a smart contract? It is actually not a new concept. It was first introduced in 1994 by Nick Szabo, the cryptographer who later invented the digital currency Bit Gold in 1998. In his paper titled “Smart Contracts” from 1994 (see screenshot below), Nick defines smart contract as “a computerized transaction protocol that executes the terms of a contract”. He then wrote another paper in 1996 titled “Smart Contracts: Building Blocks for Digital Markets” with a more comprehensive take on the building blocks, principles and use cases of smart contracts.

For the purpose of DeFi, smart contracts are nothing, but combination of code (that includes functions) and data (that designates it state). Smart contracts are located and run on Blockchain networks. The most popular smart contract Blockchain network is Ethereum. If we look at the historical development of total value locked (TVL) in DeFi protocols across different Blockchain networks, Ethereum has been dominant as shown below. Its share started to decrease from mid-2021 onwards with the emergence of new networks (incl. Polygon, Avalanche, Solana, etc.). Currently, Ethereum’s share remains around 65%.

One of the early pioneers of decentralized finance space is Aave, which is a lending / borrowing protocol. Aave was previously known as ETHLend until it rebranded in 2018. Below is a screenshot from ETHLend’s product page. There was one simple and clear premise: “Everyone has the same access to finance”.

This was the very premise why I got attracted to decentralized finance in the first place. Its great potential to extend of financial services to anyone and everyone around the globe, i.e. ‘financial inclusion’. Looking at the statistics such as number of wallets, volumes traded, lent / borrowed, etc. it all looks promising. Metamask, a leading self-custodian wallet regularly updates the market with their monthly active users (MAUs). The latest official figure was from their Series D fund raising announcement in March 2022 and it was 30 million MAUs as of Jan-2022 (a 42% increase from the previously announced 21 million MAUs four months prior).

It is a staggering number! Looking at another press release from July 2022, many emerging market countries are on their lists of Top 25 markets and Top 10 fastest growing markets (please see below). DeFi represents the top source of activity in countries such as Brazil, Vietnam, Turkey, etc. However, I find it hard to assess whether what we see here is a sign of increased financial inclusion. It is not easy to differentiate those who are in it to make profit through financial speculation from those who are there to access essential financial services such as payments, remittances, credit products for real needs, etc.

A Close Look at Financial Inclusion

According to the World Bank definition, financial inclusion means access to useful and affordable financial products and services that meet consumers’ needs — transactions, payments, savings, credit and insurance — delivered in a responsible and sustainable way. Access to a transaction account is a first step toward broader financial inclusion.

The most recent numbers in the Global Findex Database as of 2021 says there are 1.4 billion unbanked people globally (this number was 1.7 billion as of 2017). And more than half of the world’s unbanked adults live in 7 countries (India, China, Pakistan, Indonesia, Nigeria, Bangladesh and Egypt).

As we all know, money transfer (i.e. remittance) is one of the most critical and problematic activities for such unbanked population. For them, cross-border remittance is mostly for sending money back home or to address an urgent financial need of a friend or a family member. In fact, looking at the data published by the WorldBank (please see below), the top 10 countries with the largest remittance inflows almost completely overlap with countries with the largest unbanked population.

Cross-border remittances are slow and expensive, hence it must be a perfect use case of crypto. In fact, according to a report titled “The Digital Currency Shift: The Cross-Border Remittances Report” jointly published by PYMNTS and Stellar Development Foundation, almost one quarter of consumers who made online cross-border P2P payments sent funds using cryptocurrencies.

As this data is from a survey conducted with US-based consumers, the figures would very likely be lower for the recipients of cross-border remittances among unbanked population in emerging markets.

Increasing the use of crypto rails for remittance would address financial inclusion at a global scale and contribute to the adoption of crypto in a meaningful way. What it takes is the same as we see in developed markets. We need to build consumer applications with good accessibility, easy onboarding flows and robust security features. Such applications would then be integrated with domestic payments, saving and investment features offered by DeFi protocols. The combined proposition would allow the unbanked and underbanked population on the receiving end of cross-border remittances to save fees, time and start participating in financial services.